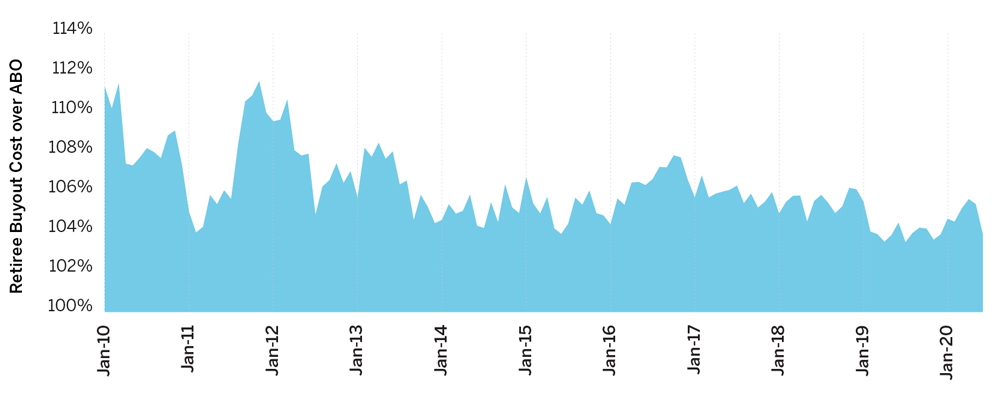

Estimated retiree buyout cost as a percentage of accounting liability decreased from 105.5% to 103.9% in May

As the Pension Risk Transfer market continues to grow, it has become increasingly important for plan sponsors to monitor the annuity buyout market when considering a plan termination or de-risking strategy. The timing of the annuity buyout can ultimately impact the cost, as well as the plan’s funding and accounting measurements. Other factors also impact annuity buyouts such as size, complexity, and competitive landscape, which should be taken into consideration with the estimated cost illustrated in the MPBI.

During May, 2020, average accounting discount rates decreased by 27 bps, while annuity purchase rates decreased by 10 bps. This caused the estimated retiree buyout cost as a percentage of accounting liability (accumulated benefit obligation) to decrease from 105.5% to 103.9%.

When considering these results, please keep the following information in mind:

- Annuity pricing composites are provided by the following insurers: Prudential Insurance Company of America, American United Life Insurance Company (OneAmerica), American General Life Insurance Company (subsidiary of AIG), Minnesota Life Insurance Company (Securian), Pacific Life Insurance Company, and Metropolitan Tower Life Insurance Company (MetLife).

- Baseline accounting obligations are estimated using a representative retiree population, the FTSE Above Median AA Curve, and insurance company data.

- Plan sponsors should note that specific characteristics in plan design or participant population could make settling pension obligations with an insurer more or less costly than estimated.

Figure 1: Milliman pension buyout index

About the MPBI

The Milliman Pension Buyout Index (MPBI) uses the FTSE Above Median AA Curve and annuity purchase composite interest rates from several insurance companies to estimate the cost, as a percentage of accounting liability, of transferring retiree pension obligations to an insurer. To review previous monthly findings, visit milliman.com/en/periodicals/Milliman-Pension-Buyout-Index.